Figuring out your years to retirement is quite easy if you start at zero net worth. The required calculation is well captured in this post.

It becomes a bit more complicated, However, if you start from a place of debt or from a place of money already saved for retirement.

Reader Ryan asked the following question a few days ago,

How do you adjust for amounts already saved? For instance, my dad is 52 and and has $400,000 in his 401k. If he is saving 20% of his income you say he has 37 more years to work. Obviously this doesn’t take into account years already worked and varying degrees of saving in those years. Please let me know if I can tweak your formula to make useful in this scenario.

Since I had already addressed this concept, I directed him back to this post.

Of course just because I had already addressed something, doesn’t mean I’d already addressed it thoughtfully. And in answering Ryan’s question I begin to feel a slight irritation in the back of my brain that my answer had been somehow wrong.

It dawned on me that I was using linear math to try to solve a problem that involved the logarithmic accumulation of compound interest.

So I went back to check my math And found that I was indeed wrong.

Sorry Ryan.

So let’s figure out the right method to answer to Ryan’s question, shall we?

We are missing one variable in Ryan’s question, of course, and that is the amount of money a year that his dad lives on. For the sake of this problem let’s assume that his spending each year is $50,000, and his take-home pay is $62,500 (50,000/80%) a year. we will also assume that his $400,000 401(k) is invested in a low-cost total stock market fund such as VTI with an assumed future annualized real return of 7%.

So let’s list our variables.

Savings: $400,000.

Yearly savings percentage: 20%.

Goal retirement nest egg: $1,250,000 *

Yearly savings amount: $12,500

Monthly savings amount: $1041.67

Using my old logic, solving this problem was rather easy, and required only mental arithmetic.

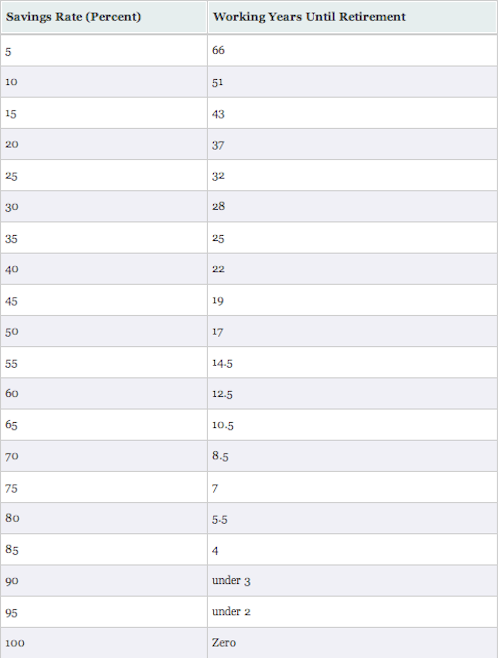

Step one was to look up a 20% savings percentage on the following chart. Which gave us an expected 37 years to retirement.

Step two was to divide his current nest egg by his yearly spending requirements. So he already had eight years of retirement income saved. ($400,000/$50,000).

And step three was to subtract his years of retirement already saved from his years to retirement. So the answer using this method was that his father had 29 years until retirement.

Which is insane. This assumes that his invested $400,000 would be worth the exact same amount at the time of his retirement 29 years from now! And that all future savings will likewise earn no compound interest. What about all the interest that he will have accrued by then though?

So let’s use our friend the financial calculator instead to right this dreadfully wrong assumption.

Plugging in our variables we can see that my initial estimate was wildly pessimistic.

Using the assumed years to retirement of our old calculation we see that in 34 years Ryan’s dad will have a nest egg of just under $6,030,000!

So what is the real answer?

Well, plugging in 13 years gets us just under the $1,250,000 nest egg necessary to keep Ryan’s father’s current lifestyle going into perpetuity.

So I was only off by less than 300%. No big deal.

Which is kind of a good news/bad news situation.

So… the bad news:

1. My initial seat of the pants method for taking into account net worth when figuring out years to retirement was totally and embarrassingly wrong.

2. My credibility in all things math has been seriously damaged by this revelation.

I’m available for tax advice too.

And the good news:

1. My old method vastly underestimated the power of compound interest.

2. Because of this if you previously used my old method to figure out your time to retirement you will likely find that you are either insanely rich by the time you retire, or surprisingly young by the time you reach your required nest egg for early retirement.

* This number is well explained in this post.

4 Responses to “Fuzzy Math”