I feel a little bit like a fundamentalist preacher who woke up one morning and realized he did not believe in God. Or not so much that he didn’t believe in god, more that he found he also believed in a larger, cooler, non Judeo-Christian god.

Up until this point I’ve done a pretty decent job of towing the company line.

And if anyone were to ask me for advice on how to invest their retirement money, I would still recommend without reservation a simple blueprint.

- Assess your risk tolerance and then assume you’re a little bit less risk tolerant than you think.

- Figure out the percentage of bonds in your portfolio that corresponds to your desired level of risk.

- Figure out whether or not you want to diversify internationally, and if you do want to, how much international exposure you desire.

- Figure out if you want to tilt your portfolio to factors like small size, value, momentum, and quality, which have all been associated with increased returns in the past.

- Invest in low cost index funds that give you appropriate exposure to bonds, international and domestic stocks, and the factors you are interested in.

- Rebalance at least once a year.

- Write your investment plan down on paper, and don’t deviate from it.

- Don’t change your plan unless there is a major life change that alters your risk tolerance.

And that’s about it. Simple, rational, and effective. Boring in the best way possible.

Boring like wise old Jack Bogle.

Have I ever showed you my rare stamp collection?

That’s (almost surely) the best way to invest. I’m convinced of it.

But I recently decided not to take my own advice. Not to stick to my own plan. Not to keep on patiently drawing base on balls and hitting singles.

I found I wanted to do the stupid thing. I wanted to swing for the fences and try to swipe a bag or two.

I’m leaving the reservation and betting my retirement on black.

And why am I doing this?

Momentum made me do it.

Momentum in investing, as you will recall, is The observation that assets that have recently done well, will continue to do well.

And there are many reasons why am a big believer in momentum.

First, on a fundamental level, it is a wager on human irrationality. And there are a few things that I believe in more blindly than the intrinsic irrationality of human decision-making. I see evidence of such heuristic thinking in myself every day and in everyone around me.

And one of the most convincing pieces of evidence about the power of irrationality, is that becoming more aware of it’s pervasiveness (by reading books such as Thinking Fast And Slow,) has not altered my own tendencies towards irrationality in the slightest.

You could say I’m bullish on human stupidity because I look at it in the mirror every day.

Second, the study of price momentum finds evidence of its pervasiveness almost everywhere it has been looked for (in most domestic and foreign asset types dating back to 1801.)

I’ve written about the simple ETF momentum strategy in the past. And have actually adopted it in my HSA account to good effect using fee free ETFs.

(it’s returned a little bit more than 10.5% since the middle of April and despite a recent downswing relative to the S&P 500, is running neck and neck with a 100% S&P portfolio.)

Now if this strategy were possible within my 403B plan, I likely would’ve converted some of my retirement money into the strategy a few months ago. But the fact is I do not have access to all of the funds needed to make this model work.

So up until now I’ve just kept on keeping on. I’ve stayed the course. I’ve indexed in low-cost mutual funds and ETFs. And I’ve maintained a portfolio style in keeping with my investment policy statement.

But then Mike from thewholestreet.com introduced me to this website. And I’ve never been the same.

Gary Antonacci is a momentum savant. He is a true believer who both manages money using momentum strategies, as well as writes beautiful academic papers showing back tests of his models.

He has a second finance book on momentum strategies coming out in November, (and I am on the waiting list for a pre-ordered a copy. Can’t wait)

His main approach is to combine absolute momentum with the more commonly described relative momentum.

“Relative momentum” essentially bets that the most successful assets or asset classes of late (relative to other assets) are likely to be the most successful in the near-term.

“Absolute momentum,” on the other hand, is the bet that no asset is worth investing in if it hasn’t beaten a risk-free investment (T-bills) of late.

Combined together these two strategies form “dual momentum.”

Relative momentum is first used to pick between two assets with imperfect correlation (like US and foreign stocks as an example.)

Absolute momentum is then used to make sure that the winning asset has had a greater total return than T-bills over the predetermined look back period (somewhere between 5 and 12 months).

Relative momentum boosts returns during bull markets, and absolute momentum arrests drawdowns during bear markets.

And while I like what relative momentum does, I love what absolute momentum pulls off.

I have been furiously back testing the strategy for the last few weeks and in general when you combine 2 uncorrelated assets and invest in them based on dual momentum, your total return is as good or better than the total return of the more successful asset during the back test, and the drawdown (The percentage of money lost from peak to trough of a Bear market) is significantly reduced (often by about 50%.)

Over time this combo seems to create a terrific melange of improved annualized returns with greatly diminished risk.

This means you can create a portfolio which is much more aggressive than your risk tolerance with much less downside risk.

So what’s not to like? Improved return? Decreased risk? I’ll report back based on my future experiences, but in looking at back tests this is what I’ve come up with so far:

Tracking error: You will often beat the market, but some weeks, months, and years you will lose to the market. Misery loves company, but you wont have any.

Volatility: Diversification means combining uncorrelated assets to smooth out the ride (up-and-down) of the stock market. Momentum means choosing one or the other based on timing. By definition the ride will be less smooth and there will be atypically violent price movements up and down. This will be painful. Worse, prospect theory reminds me that the movements down will be more painful than the movements up will be pleasurable.

Swimming upstream: To manage my money in this way is an extremely contrarian move. Every online screener will tell me my portfolio is horribly undiversified. All of my fellow Mustachians will laugh at my hubris and accuse me of market timing (and they will be right.) I will have set myself alone on an island away from my friends. This will all make periods of underperformance even more painful.

But in the end the siren song of truncated drawdowns and improved returns is simply too much for me to resist without giving it a shot.

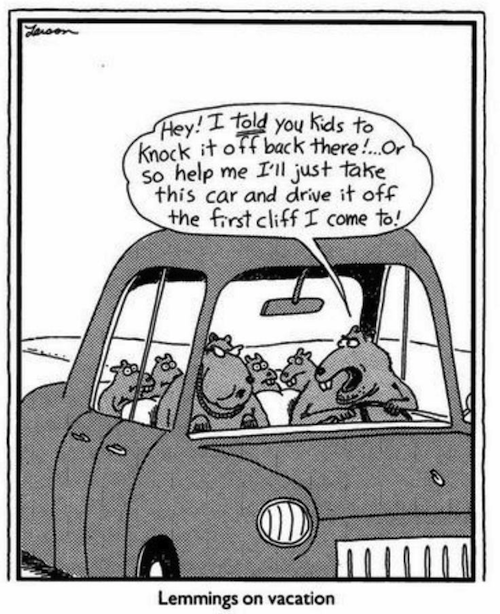

But please do not follow me down this rabbit hole. This is my own private rabbit hole. And for every solitary genius there are 1000 suicidal lemmings.

Don’t be a lemming.***

***If I wanted you to follow me off of this cliff I probably would have included a sexy total returns chart in the post…

5 Responses to “Jumping off a Cliff”