So where were we?

We’ve discussed the surprising importance of minimizing the loss of capital, and how not losing your capital ends up being much more important in the long run than finding extra returns in the stock market.

We’ve talked about the importance of diversification for buy-and-hold investors, and how the aggressive diversification across asset classes can shield passive investors from major unpredictable events, no matter what those events may be.

So today I want to describe a different passive investment approach also designed to shield the investor from large losses, while preserving respectable compounding gains.

But this strategy is a little bit unusual. If the permanent portfolio is uncomfortable, that is simply because its diversification is so aggressive. In other words at any one time a permanent portfolio investor is likely to have at least one or two asset classes that are doing terribly. But on a conceptual level it’s pretty intuitive. By owning many different non-correlated assets, one can expect not to be hurt too badly when unpredictable and destructive events happen to one or 2 asset classes.

The strategy that I will talk about today is called “barbelling,”and it is not nearly so intuitive.

But before I get into the specifics of barbelling, I wanted to circle back and talk one more time about diversification, and how it works.

And to do this I want to imagine two scenarios. In the first scenario I, as an investor, own one companies stock.

Let’s say I invest my entire fortune in the ACME Widget Company.

Investing all of one’s wealth in a single stock is about as concentrated as a portfolio can get.

So what can one expect from such a concentrated portfolio?

The most likely thing is that the stock performs on a similar trajectory to how it’s performed in the last 5 to 10 years, and the stock price moves accordingly upward at a predictable pace.

But what happens if the CEO gets caught embezzling money? The stock price can crash overnight and the company can even go bankrupt.

Contrarily, what happens if the company gets bought out by a larger company after one of its promising widget patents is approved? Well, the stock can double or triple in a very short period of time.

In other words if one has a concentrated stock portfolio, there’s a high likelihood of very bad outcomes, or very good outcomes occurring for idiosyncratic and unpredictable reasons.

Compare this to a second investing strategy where I as an investor simply buy an index of the entire stock market.

Despite the fact that wonderful and terrible idiosyncratic events are continually happening to companies in the index all the time, these good and bad events cancel each other out and I am simply left with the risk of the stock market itself.

With such a strategy I am both much less likely to double my money overnight, and to lose all of my money overnight. (And since losing all of my money is a much worse outcome than doubling all of my money is a good outcome, this diversification effect is a beneficial thing most of the time.

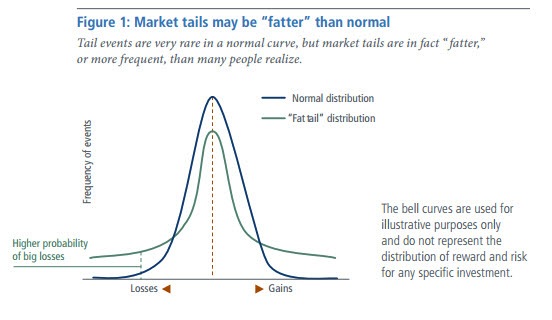

Visually, this diversification effect can be seen as a “normalizing” of the probability bell curve.

In the simplified graph below the green line represents an under diversified portfolio (like the ACME Widgets portfolio), and the blue line represents a diversified portfolio (like a broad index fund).

Imagine events on the right side of the graph being “good events” (Like making lots of money), and events on the left side of the Graph being “bad events” (like losing lots of money). And events in the middle of the graph represent average events (like slowly making money.)

Events on the edges of the bell curve are events that are simultaneously unlikely to happen, and likely to have a profound effect on one’s portfolio should they happen. These unlikely events are called “Tail events,”and the increased probabilities of tail events in the case of under-diversified portfolios are called “fat tails.”

Simply put, diversification decreases the probability of tail events and whittles down “fat tails. ”

So why waste all of this time talking about diversification when today’s topic is barbelling?

Because the whole purpose of barbelling is to take the probability curve for a diversified portfolio and and “normalize” it even further. In other words the idea is to take average events and make them much more likely, and take tail events and make them much less likely.

And how exactly does one do this?

Instead of constructing a moderately risky portfolio, one chooses to construct a portfolio which is composed of a mixture of a lot of low risk/low reward assets, combined with a tincture of high risk/high reward assets.

Larry Swedroe has written about barbelling extensively. In fact his namesake “Larry” portfolio is little more than a barbelled stock/bond portfolio.

He writes about this approach extensively in his most recent book, Reducing The Risk Of Black Swans.

What he advocates for is to take a minority of highly volatile, high expected return equities , (he argues for the stock portion of the portfolio to be invested entirely in domestic and international small cap value funds, and an emerging market value fund) and the rest of the portfolio to be invested in safe US treasuries.

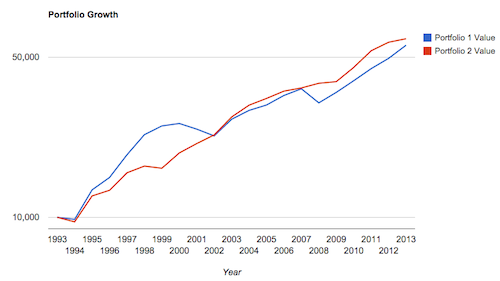

To simplify this approach let’s compare the generic moderate risk portfolio (60% S&P 500 fund/40% long-term treasury : Portfolio 1:), with a “barbelled” 30% US small-cap value fund/70% long-term treasury fund portfolio (Portfolio 2:).

(Portfolio 1’s stats above Portfolio 2’s)

These results are impressive, aren’t they? That is the magic of the barbell. By mixing in a little bit of high volatility high return stocks, with a lot of low volatility lower expected return Bonds, we are able to achieve a slight improvement in overall returns and and a marked improvement in downside protection.

Some observations:

- Note how badly portfolio 2 underperformed from 1993 to 2001. That is called tracking error, and tracking error is painful. Do you think you would’ve been able to stick with the plan in 2000?

- Look at the peak periods of outperformance for portfolio 2: 2001 and 2008. This approach wins by not losing. (Ringing any bells?)

- For further reinforcement of the benefits of this coward’s approach, compare the maximum drawdowns and worst years of these two approaches.

And some final disclaimers.

- I am not currently using, nor have I ever used such a barbelling approach for my own personal investments.

- The performance of the last 21 years tells us little about the performance of the next 21 years.

- Such an approach requires the firm belief that the size and value equity premiums will continue to exist into the future. If you are not convinced of this there is little chance you’ll be able to survive the long periods of underperformance that are inevitable with such an approach.

- Many are fearing a coming bear market in bonds given today’s low yields. One could tailor their approach to such a concern by investing in intermediate duration Bonds or TIPS, or even a barbell of short duration bonds mixed with a minority of long duration bonds. (With such an approach one would need to take more risk with stocks (perhaps a 40% small-cap value/60% intermediate term treasuries portfolio?)

- The real point here is that barbelling derisks portfolios, by avoiding big drawdowns. (And avoiding drawdowns is damned important!)

As always comments, questions, and disagreements, are welcome below.