How much money do you need to retire?

Whenever I’ve wondered this before I’ve ended up staring blankly at complicated retirement algorithms which asked me to estimate my cost-of-living in the future, future expenses, health care and education liabilities…. At some point I figured, “Aaahhh, this stuff is unknowable I’ll just max out my 401(k) and be done with it.”

But what if there were an easier way? What if you could figure out the exact number of years of you need to work in order to retire with a simple back of the napkin calculation?

It turns out there is.

A couple of months ago I stumbled upon a post by Mr. Money Mustache entitled “The shockingly simple math behind early retirement.” He expands upon an equation from “Early Retirement Extreme” by Jacob Fisker.

In short the message is this; if you know the percentage of your take-home pay that you save, you can calculate the exact number of years of employment needed until your retirement

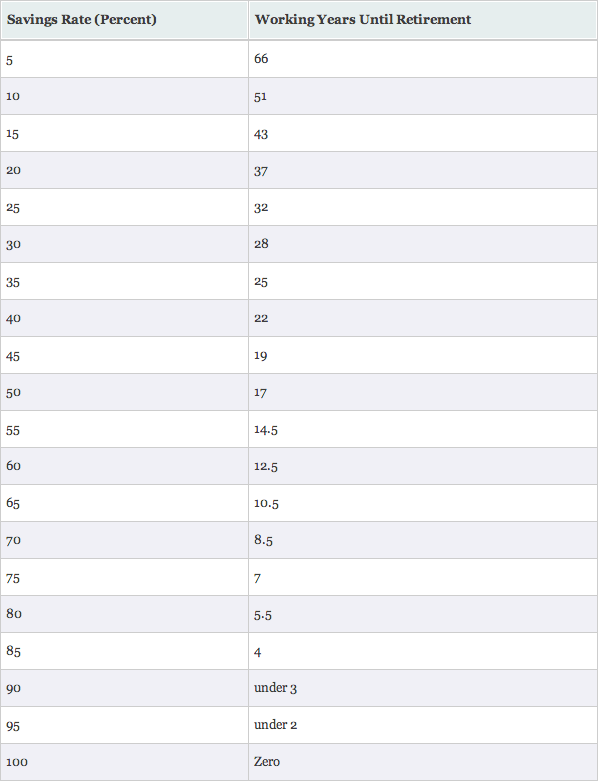

Have a look at this chart (courtesy of MMM.)

click to enlarge

It’s shocking isn’t it? If you save 5% of your take home income, you have to work 66 years to retire at your current standard of living.

If you save 20% of your take-home pay, you will have to work 37 years to reach retirement.

If you save 50%, you only need to work 17 years (ie a teacher who starts working at age 22 and saves at this rate, will be able to retire at age 39! with no change in her quality of life. )

There are more excellent points made by Mr. Money mustache in his post:

- By cutting out unnecessary things (think cable television, Starbucks lattes,) it’s fairly easy for someone with a moderate income to bump their savings percentage up significantly.

- By extension that daily latte doesn’t really cost $2.75, it costs three extra years of working full-time.

- Cutting spending is more powerful than increasing income because:

- Invested savings increase exponentially due to compound interest. and…

- Saving makes your current cost-of-living less which means you will need less in order to maintain the same cost of living in retirement.

Some additional points about why this is so exciting (to me);

- This is an empowering message. It says that your financial freedom is dependent upon something that you, in almost all cases, can influence; your own spending habits.

- The message is very democratic. You’ll notice that the amount of income you make has no place in this equation. (Note also that NFL players who make ridiculous amounts of money are often broke five years after retiring. Why?……because they spend too much money.)

- It reframes consumer culture. Maybe it’s not a good idea to buy that BMW because you can afford to make the monthly payment. Even though advertisers, friends, and the whole culture are telling you that it will make you happy, the better question is, “will it make you happier than three years of not needing to work?”

- Saving becomes pleasurable (honestly). It Is reframed not as a deprivation of current pleasure, but as a down payment on future freedom. And when something constructive becomes pleasurable, I would suggest that the likelihood of future success increases dramatically.

- The message is essentially nonjudgmental. If you’re happy working indefinitely and enjoy spending 100% of your income, then go with it. If, on the other hand, you note that your spending does not necessarily correlate with your happiness, then this gives you something else to focus on and work towards that has the potential to deliver much more happiness.

- Simply put, unless you are ridiculously wealthy, the choice to consume is likely an active choice for “things” and against “freedom.”

Personally, being a doctor, I experienced an interesting financial trajectory where for most of my 20s-30s I made a lower middle to middle-income salary, and then suddenly when I went into practice, I became a 1 percenter. Not having to worry about money definitely made me happier. The purchases really never did. In fact when making a big purchase I often experienced a sense of dread and anxiety. Buyer’s remorse.

Investing my non essential money, on the other hand, gives me no anxiety at all. I feel like I felt when I was studying hard in medical school. I’m making a down payment on my future and it feels quite good.

4 Responses to “WARNING: This Post May Change Your Life….”